Not Just a Bunch of Hocus Pocus: How the Sanderson Sisters Could Have Benefited from Estate Planning – California Legal Guide | CPT Law Read More »

Estate Planning for California Residents: Why Everyone Needs a Plan to Protect Their Family Read More »

California Estate Law Widow loses inheritance after challenging tycoon’s ‘one shekel’ no-contest will – California Legal Guide | CPT Law Read More »

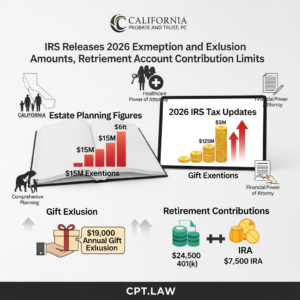

IRS Releases 2026 Exemption and Exclusion Amounts, Retirement Account Contribution Limits Read More »

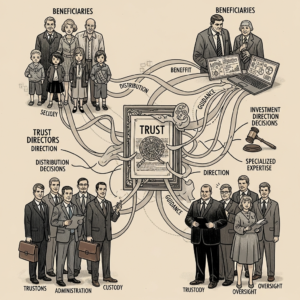

Understanding Directed Trusts in California: A Guide for High-Net-Worth Families Managing Complex Assets Read More »

Estate Litigation Prevention Aaron Carter’s Mom Claims His Ex Made ‘Illegal’ Withdrawals From Accounts, Ex Denies – California Legal Guide | CPT Law Read More »

Estate Litigation Prevention The Looming Taiwan Chip Disaster That Silicon Valley Has Long Ignored – Read More »